No guarantees

Macro elevates/ Data poor

In this report: Jeffrey Sachs breaks down the Euro/Ukraine/Russia/US situation. Big calendar week, Macro thoughts, Trade analysis on VIX, ES inc C.O.T, Gold, US 10 Year, Heating Oil.

March book recommendation: The Inner Game of Tennis: The Classic Guide to the Mental Side of Peak Performance -Timothy Gallwey

‘Europe will be forged in crises and will be the sum of the solutions adopted for those crises.’- Jean Monnet. European Union’s founding architect

Europe faces a defining moment in its meeting with UK and Ukraine leadership tomorrow in London. The choice is stark: continue military aid to Ukraine, effectively prolonging the conflict, or strategically align with the U.S. administration’s push for a ceasefire and economic deal. Any half-measures or indecisive actions could prove disastrous—both for the economic stability of the EU and the safety of Ukrainians. Europe needs its own army. If the bloc votes to roll in 100% and increase military aid behind Zelensky, they are therefore signing up to a broader war that is unwanted. All because NATO wants to have Ukrainian and Georgian missile sites. You make the counter argument to me- a European.

Contrary to the narrative pushed by some, the U.S. proposal is not a simple plundering of Ukraine’s natural resources. As detailed by the Center for Strategic and International Studies, this agreement would see both the U.S. and Ukraine sharing in future profits while also ensuring that financial aid provided by the Biden administration is repaid.

It’s frustrating to hear misinformed rhetoric, like that of Ireland’s People Before Profit representative Ruth Coppinger on RTÉ Radio 1 this past Saturday, dismissing the deal as wholesale exploitation. Unfortunately, this kind of framing is likely echoed across Europe, distorting the reality of what’s at stake. I find it downright disgusting that politicians either don’t bother to read the economic agreement details, or they are pushing a false narrative. Either which way, it shows a complete lack of integrity. Something we are thin on everywhere.

‘‘The agreed upon framework does not designate the rights of $500 billion worth of minerals revenues to the United States nor does it include a security guarantee for Ukraine’’ - Center for Strategic and International Studies

The 70 year long U.S. global policy i.e the Trump era is unwinding fast. Do you want to hold onto that? Has it served the world well? War is big business—never lose sight of that while you cheer on Ukraine to keep fighting for a part of the country they were bombing but 10 years previously? Both sides are sending troops as young as 18 years old to the front lines.

If there’s one source of clarity in the increasingly complex landscape of global policy shifts, I’d urge you to follow Jeffrey Sachs. Subscribe to his newsletters here. For years, I’ve observed his insights, and I see him as the equivalent of Elon Musk in the realm of global politics and power. What he doesn’t know about geopolitical strategy and policy simply isn’t worth knowing.

I strongly encourage you to watch the video below in full—it will give you a deeper understanding of the world as it stands today above ANY OTHER source. I can confidently say this is one of the most important speeches and Q&As for our generation to watch. It is important as we are on the precipice of a massive shift away from global hegemony to a brave new world.

Calendar

This is A BIG WEEK!

In the week ahead NFP is the main show on Friday with precursors of ADP’s and an ECB Interest rate decision. We have seen the US services data slipping into contractionary territory, so this deserves attention on Wednesday. I think there will be little respite for the market at large all week, more than any other time this year so far, given that we are coming off best levels on equities with diminishing economic data in US. Then we also have Canadian and Mexican tariffs due to be deployed March 4th/Tuesday with another 10% added-Maximum pressure! Expect volatility as the two countries sound responses on Monday. As we saw in earlier looming tariffs, it came down to a window of 12 hours before they were averted.

US economic data has been poor this year, emphasised week by week.

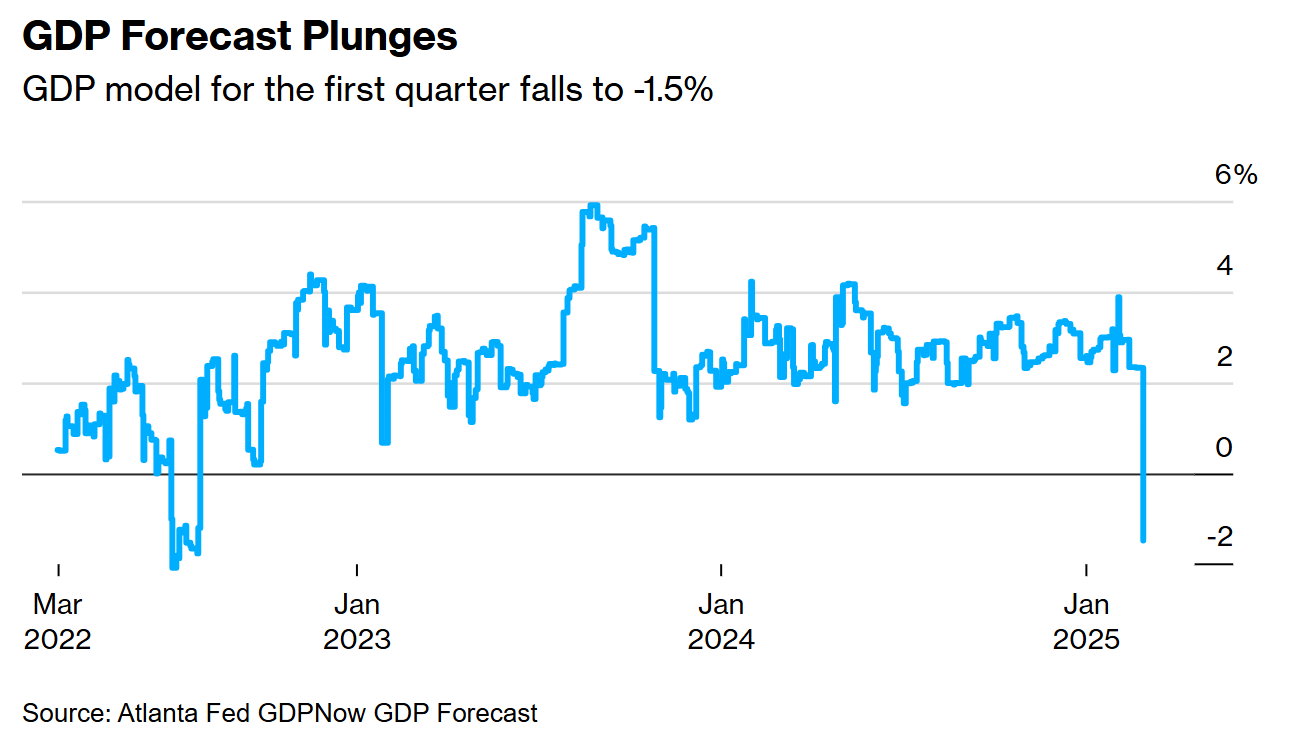

Atlanta Fed GDP Now came in a whopping -1.5%. This is down to front loading by manufacturing and retailers ahead of tariffs. If we get a weak NFP, you will see bond markets and gold start to price in a weaker Q1 2025 GDP end figure.

US consumer confidence data MISS 98.3 Expected 102.7, PRIOR 105.3.

Building permits dropped with a reading of MISS -0.6% for Jan.

Initial jobless ticked up to BEAT 242k Expected 222k

PCE Q4 Prices ticked up BEAT 2.4% Expected 2.3% prior 1.5%

Pending home sales dropped MISS -4.6%

Positive news that personal income ticked up BEAT 0.9% Expected 0.4%

EARNINGS

Costco and Crowdstrike leading the pack of mainly non-interesting market movers this week. Full list here.

Macro

Negotiations on the Ukrainian/US side have failed for now, marking the first attempt to bring all parties to the table. However, the cold reality will soon set in for Zelensky, likely tempering tensions. Europe is in no position to sustain Ukraine financially or militarily unless Germany significantly increases its defense spending and a broader shift toward higher military expenditures takes hold across the continent—an outcome that would lock us into a multi-generational confrontation with Russia.

The very bureaucracy that has long upheld European democracy—through checks, balances, and a federated system—now acts as a major headwind. This bureaucratic monolith is struggling to adapt to a shifting global order increasingly defined by fast-moving, centralized power structures, as seen in Russia, China, and the United States.

The real danger lies in Europe’s lack of a singular leadership figure capable of responding decisively to crises. Without one, the continent remains vulnerable to external shocks and slow to react. Meanwhile, internal economic pressures are already weighing heavily on key nations like Germany, Italy, and France.

Markets are unsurprisingly reacting to the downside on recent data. It is my view that equity markets will try to drastically reprice to the upside ahead of Friday’s NFP, to then potentially sell off hard on the actual data. With key auction areas in play across major markets, let’s move past the discussion and dive into the technicals.